You don’t need to lose money to learn investing. These seven costly mistakes most beginner investors make have quietly derailed thousands of new investors. But every single one is avoidable when you know what to look for.

Global equity markets have created more ordinary millionaires than any other wealth-building vehicle in modern history.

The S&P 500 alone has delivered an average annual return of roughly 10% over the past century. Markets in every corner of the world— from New York to London, Mumbai to Lagos—have consistently rewarded patient, disciplined investors over long time horizons.

Yet the majority of people still sit on the side lines, or worse, enter the market and exit at exactly the wrong moment.

Why? Because nobody told them about these seven mistakes.

Every investor, no matter how sophisticated, was once a beginner.

The difference between those who build lasting wealth and those who give up in frustration is rarely intelligence. It is almost always knowledge: knowing what traps exist before you step into them.

This article is the guide that should exist at the beginning of every investor’s journey.

Whether you are just thinking about your first investment, or you have dabbled in the market but never quite found your footing, these seven lessons could save you years of frustration and thousands of dollars or pounds, euros, or whatever currency you hold in avoidable losses.

Also Read

7 Grave Mistakes Parents Make Saving for Their Kids’ Education/Future (How to Avoid Them)

Understanding the Financial Market, Investment Vehicles and Asset Classes

Understanding the 3 Major Investment Objectives: How to Know Yours

01. The “Not Enough Money” Trap

Mistake #1—”I Don’t Have Enough Money to Start Investing”

This is the most universal excuse in personal finance—and one of the most quietly devastating.

The belief that investing is reserved for the wealthy, or that you need a substantial lump sum before you can legitimately begin, keeps millions of capable people locked out of the single most reliable path to long-term wealth.

And the longer they wait for the perfect paycheck, the more that delay costs them—not just in money, but in time, which is the one resource no amount of future earnings can ever buy back.

You may have heard the popular advice: build a skill first, grow your income, then invest.

And honestly, that advice isn’t wrong. Increasing your earning capacity is always a worthy pursuit.

But here is what that counsel quietly misses: investing is not just a financial transaction. It is a habit. It is a discipline. It is a muscle that only develops through consistent, repeated use over time.

“Capital is not measured by size. Even a single coin, invested with conviction, counts.” -Ini-Amah Lambert

If you wait until you hit your dream income before you start, you risk arriving at that milestone without ever having built the culture of investing.

The number in your bank account will have changed. Your behaviour around money may not have.

And so the same hesitation, the same excuses, the same “I’ll start properly next month” thinking that kept you on the sidelines at $500 a month will follow you faithfully to $5,000 a month.

Here is the truth: there is no wrong amount of money to begin investing with. Whether you have $1,000 or $50, the most important decision is simply to start. The return on any investment is a function of time and rate—not starting size.

A modest $200 monthly contribution, invested consistently over twenty years at an average annual return of 10%, grows to over $150,000.

The same investor who waited ten years to “save up enough first” will have roughly half that outcome—not because they invested less money, but because they invested less time.

The barrier to entry in modern markets is also far lower than most beginners realise. Commission-free brokerages, fractional share investing, and low-cost index funds mean you can own a slice of the world’s greatest companies for the price of a dinner out.

The infrastructure is already there, accessible to almost anyone with a smartphone and a bank account.

Start with what you have now—not because the amount is significant, but because the act of starting is. Every small investment you make today is also an investment in the investor you are becoming.

02. The “Big Bang” Illusion

Mistake #2—Ignoring the Magic of Compound Interest

Albert Einstein allegedly called compound interest the “eighth wonder of the world.”

Whether or not he actually said it, the underlying truth is indisputable: compounding is the most powerful force in all of personal finance, and most beginner investors completely misunderstand it.

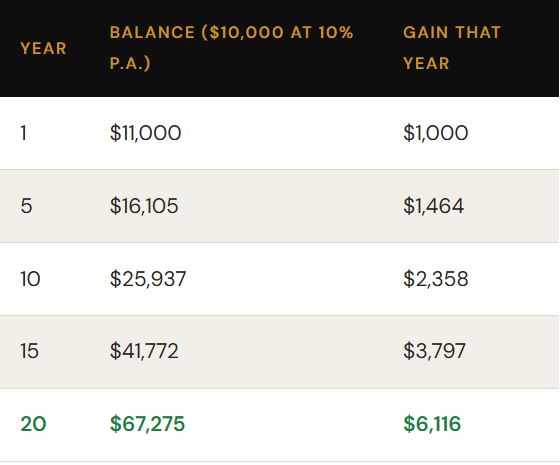

Compound interest means your returns earn returns.

When you invest $10,000 and earn 10% in year one, you now have $11,000. In year two, you earn 10% not on your original $10,000, but on $11,000—giving you $12,100.

The growth seems modest early on. But as the years stack up, the compounding effect becomes extraordinary.

This is why Warren Buffett, one of the world’s greatest investors, accumulated more than 97% of his net worth after the age of 65—not because he was a better investor in his old age, but because compound returns had decades to operate on an already-large base.

The mistake most beginners make is chasing the “big bang”—a single transformative investment that will multiply their money overnight.

This mindset leads to speculation, overtrading, and exposure to high-risk, often fraudulent schemes. The antidote is the long-term mentality: invest, stay invested, and let compounding do the heavy lifting that no single spectacular bet ever could.

03. The Ticker Symbol Trap

Mistake #3—Buying Stocks, Not Businesses

Here is a mindset shift that separates casual market participants from genuine investors:

When you buy a share of stock, you are not purchasing a ticker symbol that goes up and down on a screen. You are buying a fractional ownership stake in a real, operating business—with real employees, real customers, real assets, real debts, and a real future.

Most beginner investors forget this entirely. They chase price movements, buy stocks because they heard a “hot tip,” follow social media sentiment, or sell the moment a stock drops—all without knowing anything meaningful about the business behind the symbol. This is not investing. It is gambling dressed in investment vocabulary.

True investing begins with a question:

- Is this a good business?

- Does it have a sustainable competitive advantage?

- Is the management team competent and honest?

- Does the business generate real cash flow?

- Is it priced fairly relative to its intrinsic value?

These are the questions that the world’s most successful long-term investors—from Buffett to Peter Lynch—have always asked. The stock price is a consequence of business quality over time. Focus on the business, and the returns will follow.

Research the business before you invest. Study financials, understand the competitive position, and only invest in companies you genuinely understand and believe in.

04. The Exhaustion Trap

Mistake #4—Trying to Manage Individual Stocks Instead of a Portfolio

There is a romanticised image of the brilliant stock-picker; the lone investor who identifies a handful of winning companies, backs them with conviction, and watches their wealth quietly compound while the rest of the world scrambles.

It is a compelling story. Cinema loves it. Financial media sells it daily.

But here is what that story leaves out: even professional fund managers—armed with dedicated research teams, proprietary data, institutional access, and decades of market experience—struggle to consistently outperform broad market indices over long periods.

Study after study confirms it. The majority of actively managed funds underperform their benchmark index over any ten-year window you care to examine.

For a beginner investor working alone, with limited time and no research infrastructure? The odds are steeper still.

The real mistake, though, isn’t simply picking the wrong stocks. It runs deeper than that.

It is thinking like a stock-picker when you should be thinking like a portfolio manager—and those are two fundamentally different mindsets.

Collecting Stocks Is Not the Same as Building a Portfolio

Most beginner investors make a subtle but expensive error: they collect great stocks—and never actually build a great portfolio.

They accumulate shares in strong, well-known companies. Tech giants. Trending names. The “can’t-miss” opportunity someone mentioned on social media or at dinner.

Each individual holding looks reasonable. But there is no structure beneath it. No balance. No intentional allocation. No awareness of how each piece interacts with the others.

The result is a portfolio that looks impressive on a spreadsheet—and behaves poorly under pressure.

Think of it as a museum of stocks. A beautifully curated collection of individually great companies, displayed side by side, with no cohesion, no strategy, and no collective purpose. A museum does not need its exhibits to work together. Your portfolio does.

When every holding exists in isolation — chosen for its own story rather than its role in the whole — you are not managing wealth. You are curating a display.

Why This Quietly Destroys Returns

When you invest this way, two dangerous risks build up beneath the surface—often unnoticed until it is too late.

The first is concentration risk:

A collection of popular stocks tends to cluster around the same sectors and themes—technology, consumer brands, whichever industry is having its moment. When that sector stumbles, your entire portfolio stumbles with it.

You thought you owned ten different companies. In practice, you owned one bet, ten times over.

The second is decision fatigue:

Managing individual stocks demands constant attention—performance expectations, earnings seasons, analyst upgrades, macro news, price swings that demand a response.

The cognitive load accumulates. And when investors are tired and anxious, they make the two most expensive decisions in the game: buying high when excitement peaks, and holding on to a bleeding and bad company for too long expecting it to also perform like others.

The best portfolios—like the best football teams—win through balance, structure, and resilience.

They combine assets that behave differently under different conditions: equities and bonds, domestic and international exposure, growth and value.

When one position struggles, others hold. When one sector falls, another rises. The system absorbs shocks that would devastate a less considered collection.

Also Read

How Football Fanaticism Can Make You a Better Investor

How to Actually Build a Portfolio

Professional investors do not rely on stock-picking brilliance. They focus on three disciplines that compound quietly over decades:

Asset allocation—deciding how your capital is distributed across asset classes, geographies, and risk levels.

Research from Vanguard and others consistently shows that asset allocation explains the vast majority of long-term portfolio performance—far more than any individual stock selection ever could.

Diversification—spreading risk so that no single position, sector, or event can deal decisive damage to your total wealth.

Rebalancing—periodically restoring your intended allocation as markets shift, so that a strong run in one area does not quietly concentrate your risk without you noticing.

For most beginners, the most efficient way to achieve all three at once is through index funds, Exchange-Traded Funds (ETFs), or diversified mutual funds.

These instruments give you exposure to an entire market, sector, or asset class in a single trade. You stop betting on which player scores. You own the whole league.

You do not build lasting wealth by assembling a gallery of great companies. You build it by constructing a system — one that survives volatility, holds its shape through uncertainty, and compounds consistently across years and decades.

Stop collecting stocks. Start managing a portfolio.

Think in portfolios, not in stocks. Because in the long run, it is never the star players alone that win the championship. It is always the structure behind them.

05. The Paralysis Trap

Mistake #5—Being Too Scared to Lose Their Precious Money

Fear of loss is perhaps the most psychologically understandable mistake on this list. Nobody wants to see their hard-earned money decline in value.

But the cruel irony of financial paralysis is this: by refusing to invest out of fear of loss, you guarantee a loss—just a slower, less visible one.

Inflation is the silent tax on idle cash. When inflation runs at 5%, 8%, or higher—as it has across many economies in recent years—the purchasing power of money sitting in a low-yield savings account erodes by that same rate every year.

You may still have the same number of dollars, pounds, or euros, but what that money can actually buy shrinks relentlessly. This is a real, certain loss—not a risk, but a guarantee.

Markets, by contrast, carry risk—meaning outcomes are uncertain, not guaranteed to be negative. History shows that broad equity markets have consistently outpaced inflation over long time horizons.

Short-term volatility—the daily rises and falls that frighten beginner investors—is the price of admission for long-term returns.

The investor who can hold through temporary declines is almost always rewarded. The investor who never enters the market to avoid that discomfort loses to inflation with mathematical certainty.

Important Note:

This is not an argument for reckless speculation.

Investing in sham projects, unregistered investment schemes, or Ponzi operations is not investing at all—it is gambling with a fraudulent house advantage. Fear of those schemes is entirely rational. Fear of regulated, diversified, long-term investing in real markets is not.

06. The Prediction Game

Mistake #6—Trying to Time the Market

Market timing—the strategy of moving money in and out of the market based on speculations about where prices are headed—is one of the most seductive and destructive ideas in all of investing.

It promises the holy grail: buy at the bottom, sell at the top. The problem is that it consistently fails, even for professional investors with every conceivable analytical advantage.

The mathematics of market timing are brutal. If you miss just the ten best trading days in the market over a twenty-year period, your total returns can be cut roughly in half compared to simply staying invested throughout.

The best days and worst days tend to cluster together during volatile periods—meaning the investor who exits during a downturn to “avoid losses” is most likely to miss the sharp recoveries that follow.

Every beginner investor who has tried to time the market has experienced the same humbling pattern:

Once you sell, the market rallies without you. Immediately you buy back in, the market corrects. The transaction costs, tax events, and emotional whipsawing pile up. Frustration and burnout follow.

The professional alternative is Dollar-Cost Averaging (DCA)—a regular fixed-amount investment strategy over a long period.

By investing a set amount at regular intervals—weekly, monthly, or quarterly—regardless of market conditions, you automatically buy more units when prices are low and fewer when prices are high.

Over time, this produces a lower average cost per unit than any attempt to pick the “right” moment. It also removes emotion from the equation entirely.

07. The Knowledge Gap

Mistake #7—Not Knowing How—or Where—to Get Started

For many people, the single biggest barrier to investing has nothing to do with money, psychology, or strategy. It is simply this: they don’t know how to begin.

Either they are unaware that capital markets exist and are accessible to everyday people, or they know the market exists but find the concept overwhelming.

The jargon, the account-opening process, the fear of doing something wrong—all of it conspires to keep capable, motivated people frozen in inaction.

This knowledge gap is both common and completely solvable. Today, investing is more accessible than at any point in history.

Commission-free online brokerages allow you to open an account in minutes with a smartphone. Index funds and ETFs give instant diversification across hundreds of companies for the cost of a single share.

Robo-advisors build and rebalance portfolios automatically based on your risk tolerance and goals. The tools exist for every budget, in virtually every country.

The cure for not knowing where to start is to start learning—and then to start small.

Open an account. Buy one share of an index fund. Set up a recurring monthly contribution, however modest. The act of being in the market, even in the most modest way, is irreplaceable as a learning tool.

Real skin in the game focuses the mind in ways that no amount of passive reading can replicate.

Investing Is a Skill, Not a Lottery

None of the seven mistakes in this article are signs of stupidity or failure. They are the natural result of entering a domain without a map.

Most beginner investors make them not because they lack intelligence, but because nobody ever gave them this information clearly and honestly before they needed it.

The principles of good investing are not secrets. They are not complex. Start with whatever you have. Respect the power of compound returns.

Buy businesses, not tickers. Diversify. Manage risk, don’t fear it. Invest consistently rather than trying to outsmart the market. And take that first concrete step today.

Markets have created more ordinary millionaires than any other wealth-building vehicle in modern history—not through get-rich-quick speculation, but through the patient, disciplined application of these exact principles over time.

The question is simply whether you are going to be one of them.

Leave a Reply